Ask just about any Venture Capitalist what they think about a company and I bet you’ll get a very confident answer in return. Companies are “good” or “bad” to most VCs and fall into one of these two categories based on a variety of metrics like how quickly they’re growing, how much funding they’ve been able to attract, what the cash-on-cash markups have been, how large the addressable TAM is, what the unit economics look like and how much buzz there is in the company’s space. Lots of inputs. One output: “Good” or “Bad”.

When asked to double-click on the reasons driving why a good company is good, most VCs will share a narrative that focuses on what’s gone right which more times than not makes it seem like the company has put together a great business model and executed on scaling growth flawlessly. But ask the same Venture Capitalist to describe a good company’s weaknesses and more times than not you’ll get poor answers in return that are expressed defensively, especially if the VC is a direct investor in the firm. The truth is that every business on the face of the planet has flaws. But another unfortunate truth is that most people are more comfortable bucketing companies as “good” or “bad” than they are engaging in the dialogue that falls in the “shades of gray” category.

I bring this up because I’ve recently found myself in a number of conceptual debates about whether the recent trends in the trading space are good or bad. Reporters, VCs and Founders want to know what’s behind the growth at the notable new players and whether they’re good or bad companies. Reporters in particular want to know whether the companies are doing good or bad and whether consumers are being helped or harmed. Good or bad. Help or harm. Choose a side please and defend it to the death. And while I find Thunderdome conversations quite fun, they’re too simplistic and don’t reflect how the world really works. So instead of answering the question directly, I’m going to frame the issue by sharing my personal experiences from when I was first starting to trade. The story starts in college with a young kid (me), a 2am infomercial and a little excess cash.

To set the stage, I was a student at the University of Virginia enrolled in a five year combined Bachelor’s/Master’s degree program in the School of Engineering. My main areas of focus were Applied Mathematics, Systems Engineering and Artificial Intelligence, and I was fortunate that this combined skill set was interesting enough to the Jet Propulsion Laboratory (JPL) for them to support me while I was in school. During the school year I carried a full load of classes while working on optimization algorithms for JPL’s Mars Explorer mission, and during the summers I took a few classes while cranking out tens of thousands of lines of code. In return, JPL paid my tuition and gave me what at the time was a healthy monthly stipend of $1,250 during the school year and $1,850 during the summer months. This might not sound like a lot of money by today’s standards, but at the time I felt rich. The money was more than enough to pay my room, board and bills and go out with friends as often as I wanted to. Every month I found myself putting money in the bank.

I also didn’t sleep much in college (4 hours a night was my norm) which was great most of the time, but there were the occasional weeknights where everyone was busy sleeping and I found myself flipping channels on the TV in my room at 2am. Programming back then wasn’t like it is today. There weren’t “on-demand” services and the quality of 2am cable TV programming left something to be desired. So, as embarrassing as this is, I have to admit that from time-to-time I found myself sucked into an infomercial. 30 minutes of pure and unadulterated programming designed to get you to buy something. Capitalism on steroids. And on one night in 1990, I found myself sucked into an infomercial that was selling a system that promised to teach me everything there was to know about commodity options trading. I was hooked. It sounded like something that required analytic skills and money, both of which I felt like I had at the time. So I ordered my kit and a few weeks later I was an investor in soy bean futures.

I give you permission to laugh because it really was as ridiculous as it sounds. What the heck did I know about soy beans? Nothing. I watched an infomercial, I ordered a kit, I followed their instructions, and before I knew it I was a commodities futures investor. I had no real source of information that guided my decisions (remember that this was pre-internet) so I based my trades on historical charts I was able to analyze and some pretty questionable weather forecasts that I was able to obtain from sources in the University Library. How did it work out? I exited my first soy beans contract with a tiny loss. It was a roller-coaster of a ride so I was happy to basically get my money back. I then tried my hand at investing in corn futures and actually made a little money. This gave me the confidence to keep going. So, over the semester I ended up a pretty active commodities trader (small scale but active) and after all the ups and downs ended up losing a small amount of the money I had put to work. The loss hurt my ego more than my bank account so I didn’t have any qualms closing my account and mentally categorizing the experience as an important “life lesson”.

The second part of this story takes place a few years later when I was working at Signet Bank. I was one of the early analysts and because of my various responsibilities played a small role in the spin out of Capital One from the parent bank. Slide monkey might be the most descriptive designation for the role I played, but nonetheless I was part of the process and witnessed everything first-hand. I was part of the team that gathered financial/performance information and wrote descriptions of the different business units and outlined future risks for the S-1. We produced the physical slides that were presented in the numerous investor roadshow presentations. It was chaotic but it was also fun. And when Capital One stock started trading on the NYSE I felt like I played a part in making it happen.

This experience led a few of us to form an internal investments club with a focus on analyzing upcoming IPOs. Having just been through the experience, we felt that it would be a lot of fun to tear apart other company’s S-1s and hopefully find a few good investment opportunities along the way. The first S-1 I was responsible for leading the discussion on was Sam Adams, and to this day I remember the experience fondly. I did my homework and read everything that I could get my hands on related to the beverage industry. I learned about distribution channels and transportation costs, manufacturing margins, the power of the big beverage brands, the changing consumer preferences/attitudes towards micro-brews, the pricing power of a premium product and a lot more. The result was a personal “buy” recommendation and I was excited when I placed an order for 200 shares the day before the stock was going to officially trade. It priced at $15 and my order was executed at $20 (aren’t IPO pops terrific for the casual investor…sigh). I proudly held the stock and actively tracked the company’s progress. The microbrew fad was a real thing and Sam Adams was a good company, but the narrative wasn’t enough for the Street. Their financial results didn’t meet analysts’ expectations and new entrants were flooding the market which didn’t help the situation at all. As a result, Sam Adams stock price traded sideways to slightly down for years and I ended up selling my shares for a small loss. The stock currently trades at over $880 a share (25 years later) so maybe I should have held.

We went through this same exercise a number of times as a group and most of us built small portfolios of individual stocks along the way. The group had a lot of fun analyzing the spin-off of CarMax from Circuit City because their HQ was in our backyard. The discussion that revolved around Yahoo’s IPO was amazing because the internet was really new and as a result Yahoo had unknown but potentially massive upside. And possibly the most fun I had was investing in Zitel, a relatively unknown company that claimed to have a systemic solution for finding specific lines in code that needed to be fixed in advance of Y2K. It taught me about getting a macro issue right and riding an upwards wave that can just as quickly come crashing down when more facts surface. I rode the stock from $5 to $70 a share and back down to $3. So much fun! We eventually disbanded the group mainly due to our day jobs leaving very little time for “extracurricular fun”. And when all was said and done, the financial result I personally generated from trading in public stocks wasn’t great. The most accurate description of my portfolio would have been “2X the beta of the market with slightly below market returns”. Typical for a side-of-desk casual investor.

An infomercial and an investment club. Two very different experiences. Both with negative financial results relative to parking money in an index fund. But in retrospect, I wouldn’t trade either of my experiences for the financial returns I could have generated by “better and safer” strategies. The commodities experience taught me valuable lessons about complex financial instruments, the pros and cons of leverage and the dangers of investing without real knowledge. The investments club made me a better and more well-rounded business professional, it taught me about the importance of earnings announcements and how to value companies, and it trained me how to form a narrative about the current results and future potential of a business. My investments accounts might have been better off without these experiences but my business career and understanding of how the machinery of the stock and commodities markets work would have suffered mightily.

My personal experiences are good examples of why it’s difficult to give a simple answer when asked about the good and the bad of trading stocks and options contracts. My experiences taught me a lot when I was young and impressionable, but I’d be pressed to say that everything that happened to me was “good”. Was I in over my head in college? Absolutely. Did an infomercial convince me to invest in complex financial instruments that I should have steered clear of? Absolutely. But to be clear, I was in a financial situation where I was routinely able to save money. I was also young enough that losing a few dollars didn’t matter much. The hands-on education was irreplaceable and in the end I learned something new.

But I can imagine that there were many people who bought the infomercial’s system looking for a quick buck. The infomercial made it sound much easier and much lower risk than it was. Advertisers will be advertisers. Buyer beware. What matters is if their customers were investing precious money that mattered to their daily lives because options trading was absolutely the wrong investment vehicle for these people. I don’t have the data nor the context to know if the infomercial’s system did more harm than good, but to truly judge it one would have to study the intent and outcomes holistically. Who were they targeting (especially at 2am)? Did the system properly educate its users on the risks involved in commodities trading? Did the system try to dissuade undercapitalized and underinformed customers from investing too much (or at all)? What were their customers’ success rates? Were customers happy with their outcomes? If they had to do it all over again would they still invest in the system? Context matters.

In contrast, even though my investment club experience also produced sub-optimal financial results, I can uniformly say that it was “good”. I wasn’t in over my head. I was investing money I could afford to lose. I learned new skills that helped me in my day job. Investing gave me something to talk about other than work and helped me from time-to-time in social settings (yes – I was and still am socially awkward). All this in exchange for a few extra dollars in my account if I had invested “optimally”. But why do I see this as uniformly good when the outcome wasn’t terribly different than my college experience? I think the answer is pretty clear: As an investment group we had the skills and the ability to make good financial decisions, trust in each other’s analysis, and full transparency into each other’s trades. Our incentives were aligned such that when one of us conducted solid analysis and made a good trade recommendation, all of us had the chance to profit from that person’s work. We didn’t have to worry about pump and dump schemes. We didn’t have to pay for recommendations from each other and wonder if the recommendations matched their actual trading behaviors. Quality analysis plus trust plus transparency created a universally good experience that I valued for more than just the financial outcomes. To this day I cherish what I learned during that phase in my life.

So where does this leave me with regards to what I think about the recent trends in trading? Some of these trends I find very valuable and uniformly good. Reducing the friction and cost of stock ownership is good. The democratization of free and paid sources of information that can be used to analyze investment opportunities and understand how companies, commodities and currencies work is good. The fractionalization of shares to allow everyone to own slices of otherwise expensive stocks is good.

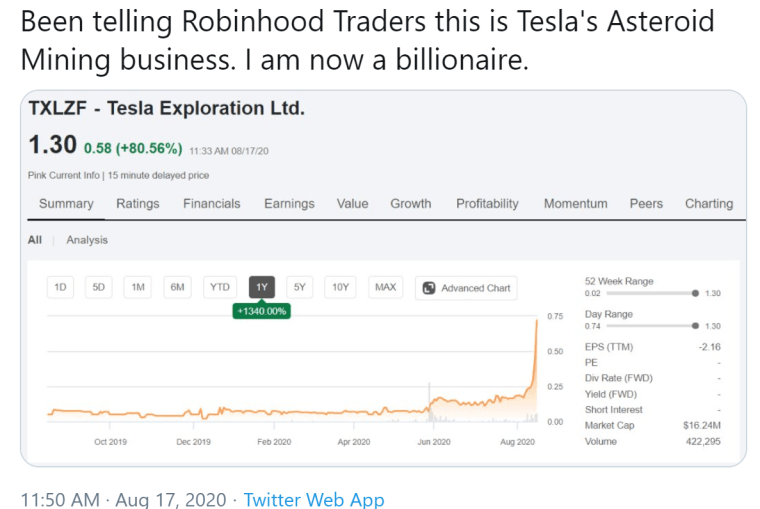

But there are also a lot of bad things happening in the ecosystem that worry me. Some free sources of information have become honey pots for unsuspecting and naive investors looking to make a quick buck on a sure thing. When information is free to share, bad things can happen that range from poor quality and inaccurate analysis being spread to outright mis-information campaigns perfectly executed with the goal of manipulating a stock’s performance. When the trading experience is overly gamified, some investors will use it as a vehicle for “hunting the quick win” and will chase the dopamine rush that comes with financial risk and real money outcomes. Take this Twitter post as an example:

The person posting is most likely joking, but the concept behind the Tweet is really troubling because Tesla Exploration has nothing to do with the Tesla electric car company nor anything to do with Asteroid mining. But a few strategic Tweets and Reddit forum posts and the stock can become a “hot buy” for all the wrong reasons. Shameful at best. Fraudulent at worst.

So where I land is that the investment space has yet to see a “perfect business model” emerge. There’s a need for quality, curated analysis and educational content that allows consumers to benefit from the trends of “free” and “frictionless”. There’s a need for more self-policing on the big platforms and methods of flagging and removing fraudulent and poor content. But, learning about and owning stocks, commodities and currencies is a good thing that should be encouraged. For many this will mean investing in generic, passive vehicles like indexed funds but for some the journey will take them down the rabbit hole and result in building a portfolio of individual investments. It’s a good practice to surround yourself with like-minded investors looking to make fundamentally sound investment decisions and to stay away from low signal echo chambers full of noise and bad (if not fraudulent) advice. Be careful about your sources and who you trust. I took the red pill and it worked out just fine for me….!!!

Very insightful. Thanks for sharing your story!

LikeLike

Thanks for the stories and insights!

I enjoy learning about industries and analyzing companies too. I am thinking about getting more active as an investor, perhaps with a medium range horizon (not day trading, I don’t have time for that).

Regarding educational content, I have been listening to the Motley Fool’s podcasts for a while, and I am considering signing up for their services. Are there other sources of analysis and educational content that you like?

LikeLike

Commonstock just relaunched and is worth checking out. Perfect place to share and find great analysis.

LikeLike

Hey Frank, great post. Thank you for sharing! I’m Hoda, founder of stockcard.io. I actually know Commonstock. David and I connected a few years ago when he just raised the first seed round. Great platform! Wondering if you’d be interested to have a discussion about the future of retail investing and how players like Commonstock and Stock Card can shape it?

LikeLike

Love the story / post, Frank. Thanks for sharing these learnings and battle scars. Some great lessons!

LikeLike